Whenever you have an ecosystem with many moving parts, even the slightest change can have lasting effects. This is exactly the case with payment processing, thanks to the credit card signature requirements being lifted earlier this year. Now, customers will no longer have to hastily scribble their autographs after every credit card transaction—a seemingly small improvement that opens the door to greater opportunities.

It’s important to point out that the signatures aren’t going away completely. Although American Express is eliminating them globally, Visa is removing the requirement only for U.S. and Canada, with Mastercard and Discover doing the same for all of North America.

Plus, the decision to do away with signatures is voluntary. If you want to preserve them for the sake of recordkeeping or personal preference, you can still do so. But if you don’t have that need, it might be in your best interest to leave the signatures behind. Let’s take a closer look at why getting rid of signatures would make sense for your small business.

How did we get here?

The payments industry has been moving toward simplicity and convenience for years. Customers want a seamless and secure way to pay for goods and services, while merchants seek reliable and flexible methods to process payments in the omnichannel era. This has paved the way to the development of innovative forms of payments, including those using near-field communication (NFC) and virtual reality (VR).

However, convenience in payment processing doesn’t always mean adding new features. Oftentimes, less is more, especially if certain features are simply no longer applicable.

On top of that, also consider why signatures came about in the first place. Back in the day, when chip cards weren’t around and the magnetic stripe had all of the important payment information, comparing the signature on the back of the card to the one provided by the customer was one of the few ways to confirm the card’s owner. Unfortunately, this practice was poorly enforced: many cardholders failed to sign their cards in the first place, while even more merchants rarely bothered to match the signatures at all.

Now that the credit card signatures are nearing extinction, let’s explore some positive effects that are likely to come out of it.

How your small business benefits

The elimination of even something as small as a credit card signature can benefit your small business immensely. Here are some of the improvements you can expect:

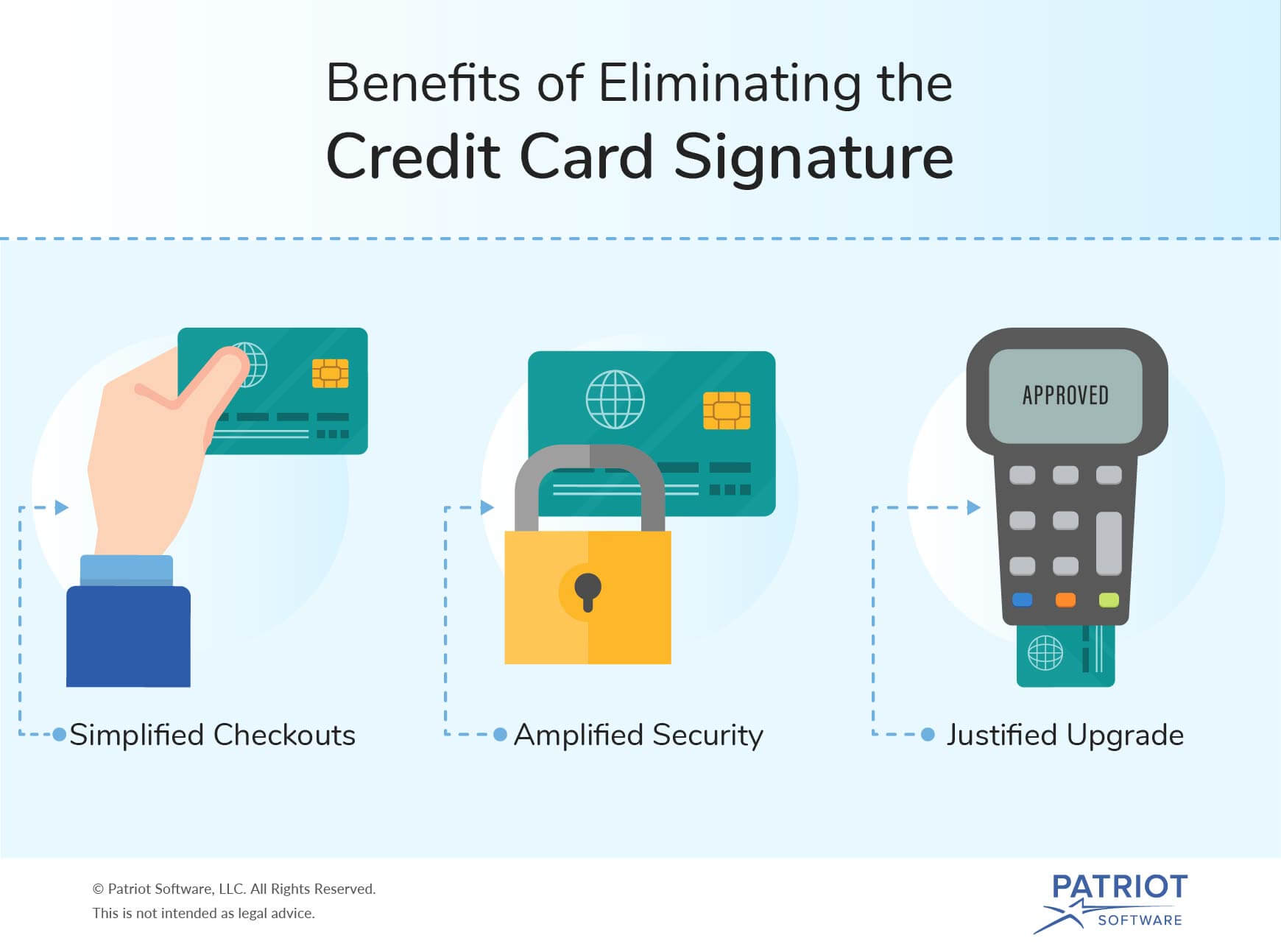

Checkouts, simplified

The elimination of the credit card signatures is a win-win for both sides of the checkout counter. As a merchant, you get to keep the line moving quickly, while your customers can expect less friction at an important point in their in-store experience.

Fewer steps to complete during the checkout may also mean fewer technical difficulties capable of preventing the payment from going through. This could prove to be one of the biggest advantages, especially on Small Business Saturday® 2018 and during the rest of the busy holiday season.

Security, amplified

If you’re concerned that the lack of signatures will allow more fraudulent transactions to slip through the cracks, remember that they weren’t doing much to prevent them in the first place. In fact, eliminating this archaic procedure gives way to newer and more effective fraud protection policies, such as the Europay, Mastercard, and Visa (EMV) standard.

The technology behind chip cards and a crucial element of U.S. payment processing since October 2015, EMV helps protect your small business from liability for fraudulent transactions and guards your cardholder data through tokenization and encryption. The former generates a unique token used in place of the actual data, while the latter converts sensitive information into a code able to be interpreted only by those with access to the right encryption key.

Upgrade, justified

Finally—and this one is important—merchants who are yet to upgrade to EMV are stuck with using the old and ineffective signature method until they complete the transition. If your small business is part of this group, and you want to make the most of modern payment processing, then you need to look into EMV as soon as possible.

After all, if the ability to accept chip card transactions isn’t good enough of a reason, then reducing security risks and avoiding unnecessary responsibility for fraud and credit card chargebacks is well-worth the one-time investment.

What’s next?

From EMV and PCI compliance to mobile payments and online credit card processing, the sunset of credit card signatures is a great reason to simplify your life even more by finding competitive payment processing. Discover how your small business can cut costs, improve cash flow, and create more opportunities for growth.

These views are made solely by the author.