One of the most important promises that small business owners make is to pay their employees on time. Covering payroll may not always be simple, but it’s vital to the well-being of the business because employees who aren’t paid don’t stick around.

When cash flow is low or irregular, however, you’re bound to have trouble issuing funds on time. How can you avoid stiffing your staff, or defaulting on any of your other financial obligations when the people who owe you don’t pay on time either?

This is where exploring forms of short-term financing comes in handy. There are a number of different lending options—some more expensive than others, or more difficult to obtain if you have a new business—that can help you stabilize cash flow in the event of late or non-payments by your clients and customers.

What is cash flow?

Your cash flow is the money coming into your business, via sales or equity, against the money going out when you pay your expenses.

Even a highly successful business with great demand for its product or service can have issues staying cash flow positive if it struggles with the timing of paying staff and bills or racks up large expenditures in order to stay productive.

Positive cash flow is important not just for covering payroll, but for taking care of all your responsibilities, such as paying rent or failing to create enough product to meet demand. But payroll is especially urgent because the people you’ve hired rely on you to pay them on time. You might be able to strike a deal with your landlord to pay rent late, but you can’t ask your employees to do the same in their personal lives.

How can financing help me cover payroll?

There are a few different reasons why your cash flow might be low even if business is going well. Your customers may not be paying your invoices in a timely fashion, or you might have made a bulk purchase on materials for inventory.

There are times when your business cash flow is going to be low, and that’s okay—it’s a part of running your business. You can make adjustments to your business model by offering early payment discounts to your clients or building up a cash reserve to help you deal with unexpected cash flow issues.

But if you find that you are constantly skirting the line between positive and negative cash flow, or you are constantly running in the red, it’s time to either drastically cut costs or explore your financing options.

Cutting costs where you can should be your first step, but when covering payroll is at risk, you may need to look into adding some additional funds in the form of a business loan.

What are your financing options?

Depending on the kind of business you own—B2C or B2B—and how often your cash flow gets low or goes negative, as well as other factors such as how long you’ve been in business and how strong your business credit score is, different financing options may work better for you.

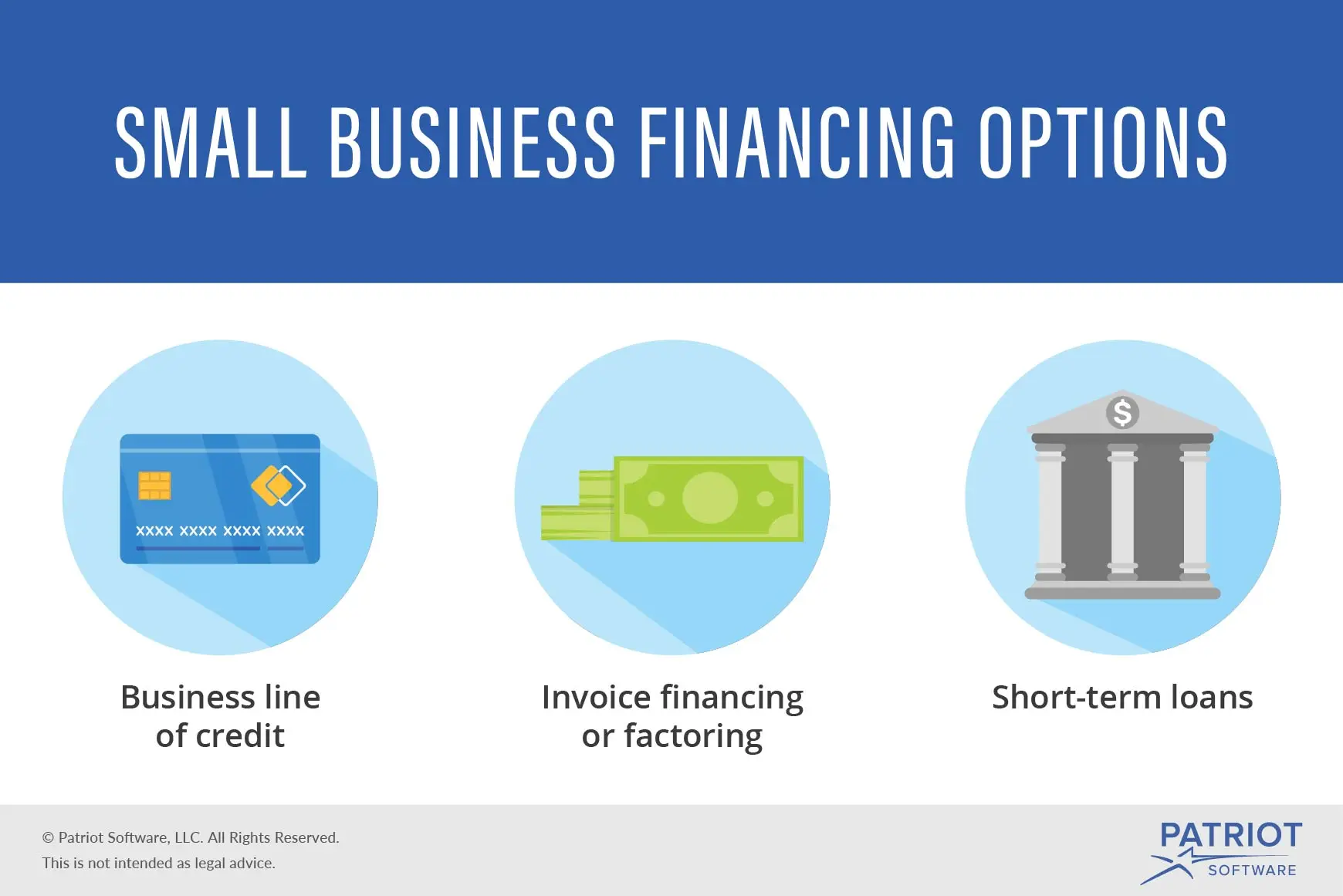

Business line of credit

Companies that have been in business for at least six months—but typically more than a year—with a good credit score and strong revenue are the most likely to be approved for a business line of credit.

A line of credit is a revolving pool of funds that a business can draw on as needed. Though similar to credit cards, lines of credit typically have larger spending limits, lower annual percentage rates (APRs), and access to cash.

If you often find yourself dealing with cash flow problems that affect not just payroll but other expenses, a line of credit is an excellent choice. You can usually use your funds for whatever you need—they won’t be earmarked specifically for payroll. And you only pay interest on what you’ve withdrawn. Say you use your line of credit often for the first few months, then don’t touch it for a while before an unexpected expense motivates you to draw on it again—you will only pay interest on the actual amount you need to withdraw against your limit.

Invoice financing or factoring

If you have a new business, less-than-stellar credit, and find that unpaid invoices are your largest source of cash flow irregularity, invoice financing can be a more obtainable option than a line of credit or term loan.

When you finance an invoice, lenders give you about 85% of the total invoice, holding the other 15% until your client pays up—minus a fee for their services, which can vary based on how long your client waited to pay. No additional collateral is needed: Your invoice secures the loan.

Invoice factoring is when you essentially sell your invoice to the lender and they assume responsibility for collecting from your client. This is a more expensive form of invoice financing, but it also removes the onus of collecting on invoices—assuming you’re comfortable lettering clients interface with a third-party when delivering payment.

Both forms of so-called “accounts receivable financing” are more expensive than lines of credit, but easier and faster for all businesses to obtain.

Short-term loans

Not every business has the business credit history for a line of credit, or the invoices that B2B companies use for invoice financing. If you hit a one-time snag in your cash flow and just need a temporary infusion of funds to smooth things over, you might consider a short-term loan.

Applying for a short-term loan through an online lender means you can be approved and funded in as quickly as one business day. When your funding need is immediate and substantial, a loan might make sense.

Keep in mind, however, that a short-term loan is likely the most expensive option of the three listed in this article, and its terms will be less generous than that of a longer term loan through a traditional lender or the Small Business Administration. Repayment is often within a year, and sometimes less, with high interest rates.

If you absolutely need funding, a short-term loan isn’t the worst thing you can do, but it requires careful planning regarding repayment, unless you want to find yourself back in the red quickly, erasing any gains you might have made.

A final word

In a perfect world, you’d never be in a position where you choose between compensating your employees or yourself or paying off your utility bill or your suppliers. Small business owners know how difficult balancing cash flow can be, however, and how often these issues arise. If outside financing helps you cover these costs while keeping your employees happy and your business healthy, it’s worth seeing what options make sense for you.

These views are made solely by the author.